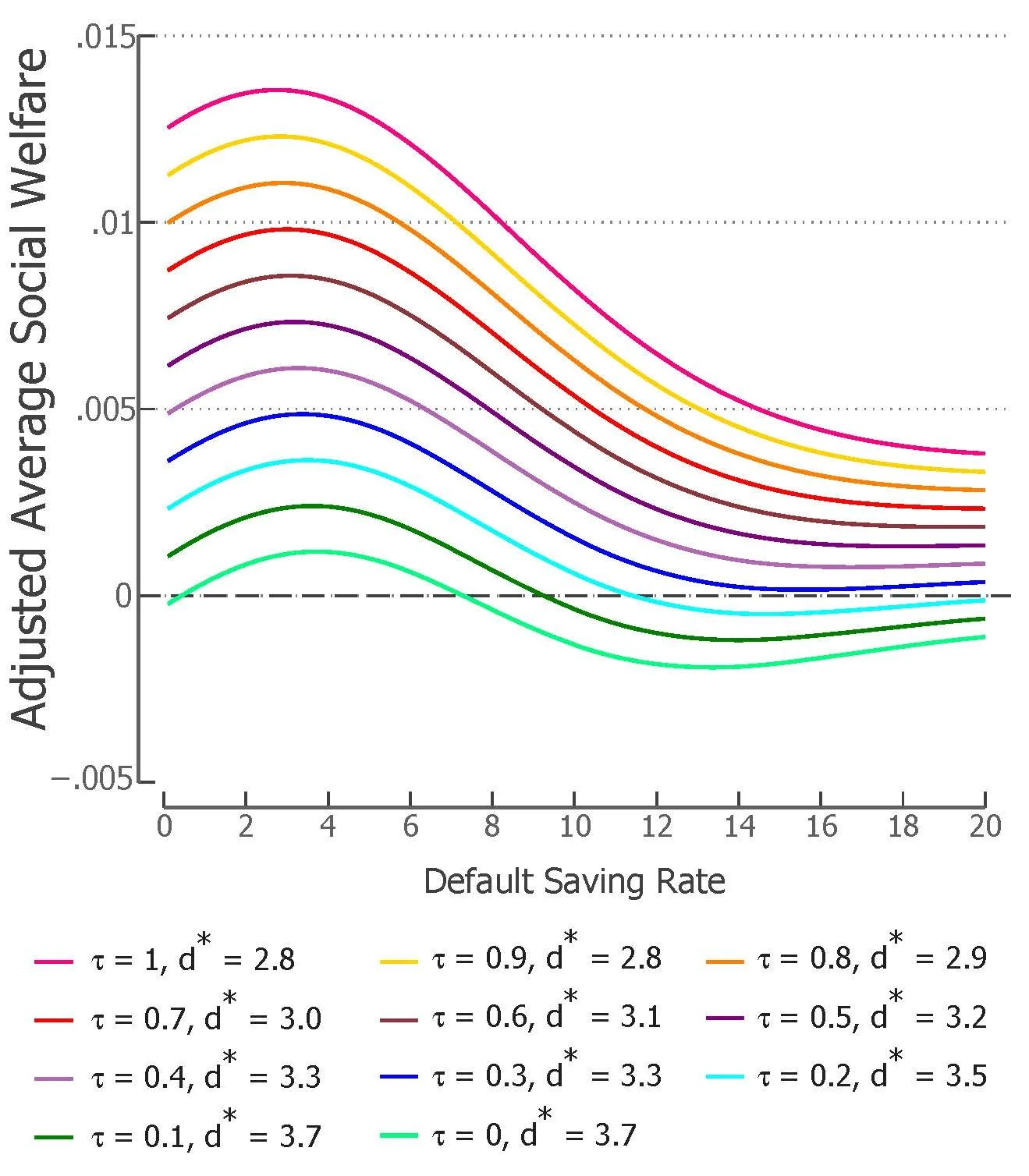

Abstract:

By assuming that passivity is exclusive to the default option, existing models of default design imply divergent optimal policies depending on whether default effects reflect welfare-relevant adjustment costs or behavioral biases. I show that this divergence can collapse when passivity is not limited to accepting the default. Using administrative tax records covering early-adopting U.S. states, I examine the default effects of state auto-IRA programs and find persistent increases in retirement savings accumulation, with participants retaining their savings even after job separation. However, increasing the auto-IRA default rate causes many participants to exit default saving and choose a zero saving rate. To explain these patterns, I extend standard models by incorporating \emph{two} competing passive options---default saving and non-saving---each associated with its own friction. I structurally estimate the model, finding the optimal default rate to be stable between 2.8\% and 3.7\%, regardless of whether frictions reflect real costs or behavioral biases. This stability arises because changes in the default partially reallocate individuals across passive options rather than inducing large shifts toward active choice. The findings recommend a narrow range of moderate default rates, even if default effects reflect behavioral biases; in this case, the default rate acts as a second-best option that mitigates other distortions to saving behavior.